Facing challenges such as learning obstacles, physical differences, hearing loss, or vision impairment can make daily life more demanding. Moreover, pursuing higher education may present additional difficulties for individuals with disabilities. Fortunately, students in such situations have various support options to explore, which can aid them in navigating college life and managing associated expenses. Scholarships, specifically designed to assist those with disabilities, can be a valuable resource in this regard. In this article, we will explore the significance and benefits of scholarships for students with disabilities and how they can make a difference in their academic journey.

Rights of Students with Disabilities

Students with disabilities are entitled to several legally protected rights. While some are aware that these rights encompass protections against discrimination in the workplace and access to services during elementary and high school, not everyone realizes that they also extend to college students. Consider these acts.

The Rehabilitation Act of 1973. This is a crucial act that prohibits discrimination based on disability in schools that receive federal funds. This anti-discrimination provision can be found in Section 504, which also grants students the right to create 504 Plans during their elementary and high school years. It’s important to note that if a school accepts federal grants, it is legally obligated to adhere to this rule.

Americans with Disabilities Act. The (ADA) is a significant piece of legislation. Under Title II of the ADA, individuals with disabilities are protected from discrimination by state and local governments, including public colleges and universities. Meanwhile, Title III requires public places, including schools, to provide necessary accommodations for disabled individuals, such as ensuring wheelchair accessibility. It’s worth noting that Title III also extends its protection to private schools that are not subject to Title II.

Does Your Condition Qualify?

Many disabilities may qualify under Section 504 or the ADA. However, not all do. The ADA defines a disability as “as a physical or mental impairment that substantially limits one or more major life activities.” The Rehab Act defines it as “has a physical or mental impairment which substantially limits one or more major life activities.” The act further explains that this can include loss of a body part, neurological conditions, mental and psych disorders, and even endocrine disorders.

So does your disability qualify? Here is a list of disabilities that may be protected by one or both of these laws. It may not be exhaustive, so students may wish to talk to a disability rights advocate to determine if they have protection:

- Deafness or hearing loss

- Blindness or vision loss

- Medical conditions like diabetes, cancer, HIV infection, or epilepsy

- Autism

- Dyslexia, ADHD and other learning disabilities

- Intellectual disabilities

- Missing limbs

- Multiple sclerosis

- Muscular dystrophy

- Bipolar disorder, schizophrenia, and other psychological conditions

- PTSD

- Mobility problems

- OCD

- Cerebral palsy

- Tourette’s Syndrome and other neurological disorders

Telling the School About Your Disability

To receive the necessary support from your school, it’s important to disclose your disability. If you’re seeking financial aid related to your disability, proper documentation may be required. Fortunately, financial assistance is available to those who qualify. Here are some useful tips to help you along the way:

Discuss Your Need with the Admissions Professional

Initiate a conversation with your admissions counselor, informing them about your disability and any accommodations you may require. They can guide you to the appropriate resources within the school.

Submit Medical Documentation

Obtain relevant documents from your doctor that confirm your disability. These documents may be necessary for both the school and any scholarships you apply for.

Submit High School Plans for Services

If you had an Individualized Education Plan (IEP) or Section 504 plan during high school, consider submitting them to the school. While they may not replace proof of disability, they can provide insight into the assistance you may need.

Ask for Help Early

Request assistance and submit the required documents early in your application process. This allows the school sufficient time to evaluate the accommodations you may require and gives you the opportunity to obtain additional documents if necessary.

Distance Learning with a Disability

Distance learning can be highly beneficial for students with special needs as it offers the opportunity to take classes from the comfort of their homes using a computer. This setup allows for breaks and flexibility in scheduling, catering to individual requirements. Moreover, the challenges of physical accommodation on campus or the difficulties of travel with a disability are eliminated.

Despite its advantages, distance learning may pose certain challenges for students with special needs. Some schools may not always be readily equipped to assist online students effectively. Additionally, not all distance learning platforms are designed to be disability-friendly. To address these issues, schools must ensure the use of technology that is compatible with assistive devices, such as readers for visually impaired students or closed captioning for those with hearing impairments. Making distance learning accessible to all students is essential for promoting inclusive education.

Helpful Accessibility Apps

Some apps can help make it easier for students with unique needs to pursue their education. Consider these:

- Speak It! This text to speech app lets non-verbal students type words the app speaks for them.

- Dragon Anywhere. This app helps students who struggle to write. It translates spoken words into written text.

- Talking Calculator. This app turns the phone into a talking calculator, which works great for visually impaired students.

- Voice Dream Reader. This tool scans text and reads it to the student, which helps students with reading and vision challenges.

- Petralex. This app amplifies sound for hearing impaired individuals.

Federal Disability Benefits That Could Help Pay for College

Students who are recipients of Social Security Disability benefits can continue to receive them even while attending school. However, it’s important to note that SSDI is typically provided to individuals whose disabilities prevent them from working. The Social Security Administration may assess whether a college student who can attend classes is also capable of holding a job. While students who reside with their parents and are enrolled full-time in college may still qualify, others might not meet the eligibility criteria. If you receive SSDI, you have the flexibility to utilize the payment for various expenses, including college-related costs.

The Importance of Financial Aid for Students with Disabilities

Living with a disability can result in increased expenses, as regular doctor’s appointments and the need for assistive devices can add to daily living costs. However, financial aid can provide crucial support for students with disabilities, enabling them to overcome these challenges and pursue their educational aspirations. It’s important to note that financial aid options are available for those who meet the qualifying criteria, offering valuable assistance in managing the financial burden and making education more accessible for students with disabilities.

Getting Help with Your Scholarship and Financial Aid Form

For students seeking assistance with filling out scholarship applications, FAFSA, or other financial aid forms, reaching out to the financial aid office at their school or their high school’s guidance counselor is advisable. These professionals are equipped to offer the necessary support and guidance needed to navigate the application process successfully.

Other Financial Aid Options for Students with Disabilities

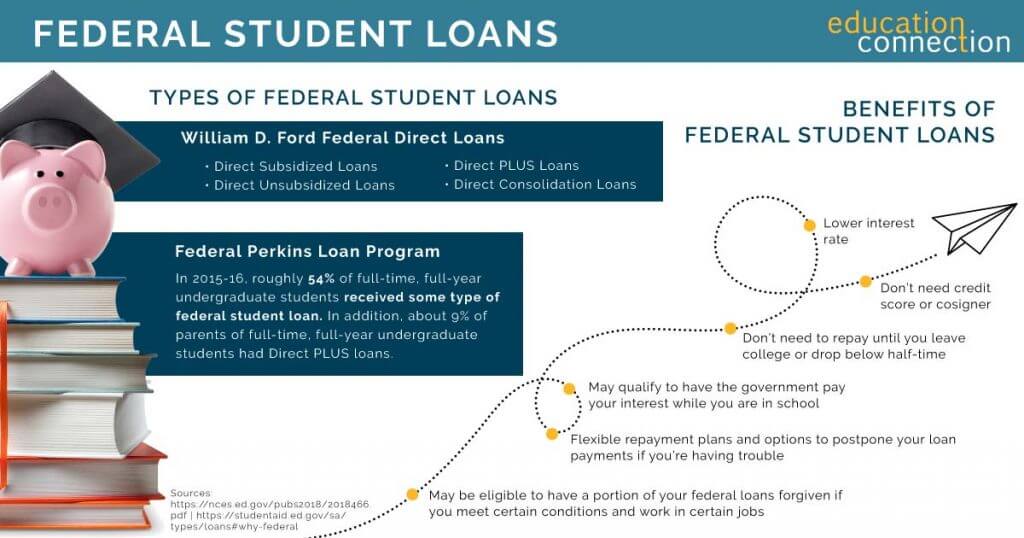

Students with disabilities have the opportunity to apply for various types of federal student aid to assist with their higher education expenses. The U.S. Department of Education offers federal student loans and grants that can provide essential support to eligible students. Some of the available options include:

- Federal Pell Grants. These are based on financial need and often do not have to be repaid.

- Federal Supplemental Educational Opportunity Grant. This grant is open for undergrad students with extreme financial need. It often does not need to be repaid.

- Federal Stafford Loans. These are based on financial needs and often do need to be repaid.

- Federal PLUS Loans. These are loans made to parents based on the family’s financial needs.

- Work-Study Programs. These programs pair students who are U.S. citizens and Permanent Residents with jobs that may help them pay for school.

- State Vocational Rehab Services. Many states have a VR office that helps disabled individuals prepare for work. This might include college level training.

Additional Resources

Students with disabilities who need additional help with school or want more info about potential scholarships should contact these groups.

- American Association of People with Disabilities. AAPD has a wealth of resources for disabled students. They have advocates who argue for disability rights and support networks for people with disabilities. Students can take part in summer internships.

- Easter Seals. Easter seals help adults and students with disabilities find services. They can also assist with getting students properly diagnosed.

- The Arc. The Arc serves people and families touched by intellectual and developmental disabilities, including 100 different diagnoses. This advocacy group provides employment programs and education support.

- Special Needs Alliance. This network of attorneys provides help for students and adults with a documented disability who need to understand their rights under the law.

- Comprehensive Transition Programs. These programs give students with intellectual disabilities help with the entire college process, from admissions to coursework. This is a federally funded program that students apply for through the participating school.

- National Center for Learning Disabilities. The NCLD provides help, support, and funding for people living with learning disabilities.

Scholarships for Students with Disabilities

If your disability qualifies for financial aid programs, there are a number of scholarships for students with disabilities to consider to help you pursue your career goals. These scholarship opportunities are a good place to start for financial assistance.

Attention Deficit Disorder

- Rise Scholarship Foundation Inc. This scholarship offers a $2,500 scholarship to students with ADHD or ADD who also have one additional learning disability. This scholarship is awarded annually and requires applicants to maintain a 2.5 grade point average.

- Anne Ford Scholarship. This scholarship provides an annual award of $2,500 for four years. It is available to eligible high school senior students with ADHD or another documented learning disability. To qualify, students must be enrolled in a full-time, four-year degree program at an accredited school. The application deadline typically falls in the fall.

Autism Spectrum

- Avonte Oquendo Memorial Scholarship for Autism. was established in memory of an autistic boy who went missing in 2013. The Perecman Firm, a law firm, initiated this scholarship, offering $5,000 annually to autistic individuals or family members of someone with autism. The application deadline is July 31.

- Kelly Law Team Autism Scholarship. Open to all individuals with autism, offering two $1,000 awards from the firm. To apply, candidates need to submit an essay detailing how they would utilize the scholarship. The selection process involves online voting, and the essay with the most votes receives the award. The deadline for essay submissions is December 20.

- Making a Difference for Autism. This scholarship is available for both high school and college students with autism. This $500 scholarship is awarded multiple times throughout the year, and students have the opportunity to apply more than once. The application deadline is in April.

- Organization for Autism Research. This offers a $3,000 award for students on the autism spectrum who are enrolled as full-time students. The next application cycle is set to open in December 2023.

- Dan Archwamety Scholarship. This offers a $3,000 award for students on the autism spectrum who are enrolled as full-time students. The next application cycle is set to open in December 2023.

General Disabilities

- INCIGHT Scholarship. The INCIGHT College Scholarship is available to eligible students in WA, OR, or CA who have any ADA, IDEA, or DSM-V defined or protected disability. To retain the scholarship, students must complete 30 hours of community service.

- AAHD Frederick J. Krause Scholarship on Health and Disability. This is designed for students with disabilities who are pursuing a full-time undergraduate program or a full or part-time graduate degree. Applicants must be at least college sophomores at the time of application, and the scholarship award is $1,000.

- AbbVie Immunology Scholarship. This group offers up to $15,000 in financial support to students who are living with inflammatory diseases, such as Crohn’s disease. The application period for this program will begin on October 24, 2023.

- Student Award Program of the Foundation for Science and Disability. This award of $1,000 is given to fourth year undergrad students or graduate students. Students must be studying STEM or computer science and must have a disability to apply.

- John Lepping Memorial Scholarship. This scholarship is specifically intended for students with disabilities. To apply, students need to submit an essay describing their disability and how it has financially impacted their family. Eligibility is limited to residents of New York, New Jersey, or Pennsylvania. The award amount can be up to $5,000.

- BMO Capital Markets Lime Connect Equity Scholarship. This scholarship offers a $10,000 education award and is merit-based, available to students with any type of disability. To qualify, students should be enrolled in four-year degree programs related to computer science, business, or a STEM field.

Hearing Impairment

- Anders Tjellstrom Scholarship. This award of $2,000 per year is open to students with Baha System implants. A GPA 3.0 GPA (unweighted) or above is required.

- Graeme Clark Scholarship. Students with cochlear nucleus implants can apply for this $2,000 award.

- Linda Cowden Memorial Scholarship. This one time $1,000 award is for deaf or hard of hearing students. They must be preparing to work in the hard of hearing community and live in middle TN.

- Sertoma’s Scholarship for the Hard of Hearing or Deaf. This is one of the top awards for hearing impaired students. To be eligible, students must have a minimum of 40dB bilateral hearing loss and be enrolled in a full-time bachelor’s degree program. The scholarship offers a generous $1,000 award.

Learning and Cognitive Disabilities

- P. Buckley Moss Foundation for Children’s Education. This award is for students with language related learning disabilities who wish to pursue college education in the arts. The $1,000 award is based on financial need.

- Guthrie Koch Scholarship. This award is for students who have PKU and control it with a low protein diet. It is open to undergrad students.

- Allegra Ford Thomas Scholarship. This scholarship fund awards $2,500 a year for two years to students attending community college with a learning disability. The deadline is in the fall.

Physical Disabilities

- 1800wheelchair.com Scholarship. This $500 award goes to students who use wheelchairs or power chairs for mobility. The student must apply by May 30. No specific disability is required.

- Disabled Student Scholarship. This $500 award is offered to any student who has a debilitating condition and wishes to pursue education. A physician’s statement of the diagnosis is needed to apply.

- Karman Healthcare Mobility Disability Scholarship. Students who use mobility devices due to their disability can apply for this award. They must write an essay and apply by Sept. 1. A GPA of 2.0 or higher is needed. The award is $500.

Tourette’s Syndrome

- Dollars 4 Tic Scholars. This program through the Kelsey D. Diamantis TS Scholarship Family Foundation awards at least one $1,000 award every year to a student with Tourette’s Syndrome. The program has two application deadlines each year, one in the fall and one in the spring.

- Kenny’s Dream Foundation. This scholarship provides up to $1,500 for college expenses for students with TS. Applicants must have a doctor’s diagnosis of the disorder.

Vision Loss and Blindness

- Fred Scheigert Scholarship Program. The Fred Scheigert Scholarship Program awards $3,000 to three students with visual impairments. Students can apply between Jan. 1 and March 15. This is a highly competitive award and requires a phone interview.

- American Foundation for the Blind. AFB offers multiple scholarships for legally blind students ranging from $2,000 to $7,500.

- National Federation of the Blind. This group has merit scholarships for blind students ranging from $3,000 to $12,000.

- Lighthouse Guild. The Lighthouse Guild awards 17 students with blindness or low vision up to $10,000 to use for undergrad or graduate training. The award is based on academic merit.

- American Council of the Blind Scholarship. ACB offers a scholarship program that awards between $2,000 to $7,500 for students who are legally blind. They must maintain a 3.0 average and be a full time student.

Schools for Students with Disabilities

While schools are required under the ADA to be accessible for people with disabilities, not all are as disability friendly as others. These are some schools to consider based on disability.

Attention Deficit Disorder

ADD/ADHD requires special tutoring and services, which can be found at these schools:

Southern Illinois University Carbondale

Visit School

A robust disability services program makes SIU Carbondale perfect for students with ADD and ADHD. It has a robust list of majors, including bachelor’s, masters, and PhD degrees. Degree programs include:

School Details:

Autism Spectrum

These schools embrace neuro diversity:

Drexel University

Visit School

Drexel University offers a wide range of social skills services to students with autism. Its Disability Resources department strives to help disabled students have a positive college experience. The school has over 120 graduate degree and certificate programs and 80 undergrad degrees. Programs include:

School Details:

- MSCHE Accredited

- Online Degree Programs: BS, MS

Daemen College

Visit School

Daemen College has a disability support service specifically for autistic students. This small, suburban school has a strong focus on the healthcare field. It has multiple majors, including these:

- Visual and Performing Arts (BA)

- Business Admin (BS)

- Social Work (BA)

- Health Promotion (BS)

General Disabilities

The disability support at these schools aims to help students with varied disabilities:

University of Arizona

Visit School

University of Arizona may be a great option for disabled students. It has over 250 undergrad programs as well as master’s and PhD level programs. Some of the degree programs include:

- Bio Chem (BS)

- Engineering Management (BS)

- Accounting (BS)

- Business Admin (BS)

Hearing Impairment

Students who struggle to hear may find these schools accommodate them well:

Gallaudet University

Visit School

Gallaudet University has specific programs for students with hearing impairment, with all courses taught in both spoken English and signed English. It is the only university that targets deaf students specifically. Other disabilities are also accommodated, and hearing students are welcome. Degree programs include:

- American Sign Language (BA)

- Education (BA)

- Psychology (BA)

- Theatre Arts (BA)

Midwest Institute

Visit School

Admission Requirements:

- High school or GED considered but not required

- Admission Rate: 100%

- Grad Rate: 90%

- Average Annual Cost: $16,645

- Median Salary After Completing: $16,700 to $29,119

Popular Programs

- Dental Assistant

- Medical Assisting

- Massage Therapy

- HVAC

Learning and Cognitive Disabilities

Learning differences require additional support at school, and these schools have risen to the challenge:

University of Iowa

Visit School

Students with learning disabilities may achieve a Big Ten college experience through the University of Iowa. This school has a disability program for cognitive disabilities that focuses on career training. Undergrad degree programs include:

- Civil Engineering (BSE)

- Public Health (BA)

- Secondary Ed (BS)

- Sports Studies (BA)

Physical Disabilities

Navigating a campus with a physical disability is challenging, but these schools strive to make it easier:

University of California Berkeley

Visit School

UC Berkeley has recently performed campus improvements to make its campus more wheelchair friendly. This means students with physical disabilities can get around campus easily. This school has over 350 degree programs across 184 departments. It holds the distinction of 31 alumni who earned Nobel Prizes. This school has many undergrad degree programs, like:

- Social Welfare (BA)

- Environmental Science (BS)

- Business Admin (BS)

- Bio Engineering (BS)

Tourette’s Syndrome

Though there are no specific programs for students with this condition at any colleges, students with Tourette’s Syndrome could find excellent support at:

West Virginia Wesleyan College

Visit School

West Virginia Wesleyan has 56 undergrad majors for students to consider. It also has four master’s programs and a Doctor of Nursing Practice option. Many programs to assist students with special needs as well as Mentor Advantage Program tutoring services could help students with TS get off to a good start. Degrees include:

- Exercise Science (BS)

- Business Administration (BS)

- Physics (BA)

- El Ed (BS)

- HLC Accredited

- Online Degree Programs: BS, BA

Disability Programs

- The Learning Center

- Mentor Advantage Program

Vision Loss and Blindness

These schools offer good accessibility for students with vision loss and blindness:

Missouri State University

Visit School

Missouri State University has 102 bachelor’s programs, 61 master’s programs, and 7 doctoral programs. Its Disability Resource Center keeps visually impaired students well informed about things that affect their navigation of campus. Undergrad programs at this school include:

- Online Degree Programs: Doctoral, MS, BS

- HLC Accredited

Disability Programs

- TRIO Student Support Services

- Disability Resource Center

University of Connecticut

Visit School

UConn has a large campus with a small student to faculty ratio. The Center for Students with Disabilities helps modify the campus when needed for students with visual impairments. The school regularly has over 1,000 students with this disability. It has 14 schools and over 100 undergrad majors, including:

- NECHE accreditation

- Online degree programs: MS

Disability Programs

- Center for Students with Disabilities