Table of Contents

What is Student Loan Forbearance?

Student loan forbearance is a short term way to pause or lower your monthly student loan payments. If you suffer from financial stress, a forbearance may offer 12 months or less of student loan relief.

Due to the pandemic, students who took out federal student aid in loans may qualify. On Feb. 1, 2023, the federal government put in place an administrative forbearance. Will student loan forbearance be extended? The program put a freeze on federal student loan payments and set the loan interest rate at 0% until Sept. 30, 2023. That means, your loan balance may not increase even if interest rates do.

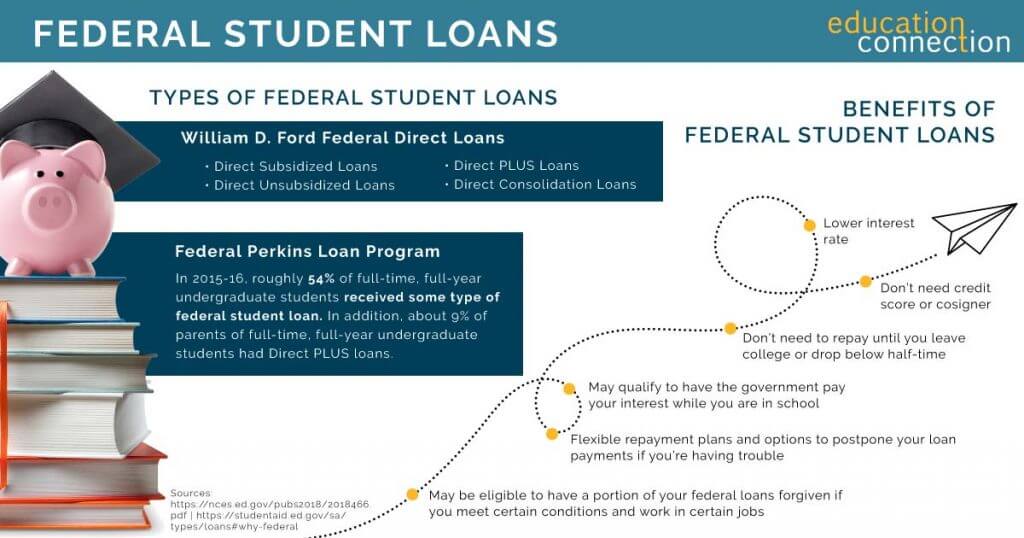

There are two types of forbearance available from the U.S. Department of Education. Each comes with a set of criteria and a form to file your request with. A general forbearance is also known as discretionary forbearance. That’s because it is up to your student loan lender to decide whether to grant your request for a suspension of payments.

If it’s granted, the period cannot last more than 12 months at a time. When it expires, you may put in a new request as long as you’re within the cumulative limit of 3 years.

Mandatory forbearance means your lender has to grant the relief. Again, for no more than 12 months at a time. If you continue to meet the terms, you may put in a request for a new one once it expires.

Private student loan forbearance is different. In general, private lenders set less flexible terms compared to federal loans and options vary with each lender. For example, a lender may allow you to make interest payments only.

How Does Student Loan Forbearance Work?

Student loan forbearance works by providing a temporary pause on paying back your loans each month. You must qualify for one and then make a request by filling out a form based on your eligibility. Keep in mind, if you’re in default on your student loans, then forbearance may not be an option.

A forbearance either allows you to make smaller payments or delay your payments for a specific period of time. As a result, unpaid interest on the principal balance adds up or accrues. Thus, each month you typically don’t pay the accrued interest.

Let’s say you receive a forbearance, but good favor hits and times get better. You could still repay your loans or even make smaller payments if this is an agreed upon option. On the other hand, if your period of forbearance ends and you’re still in distress, you may be able to reapply.

Who Qualifies for Student Loan Forbearance?

Eligibility for student loan forbearance differs with each type of loan and student loan lender. If you have a private lender, some grant a forbearance period to students who take part in a medical residency or internship. Many also offer a six month grace period after graduation. This leaves you time to find a steady job and income.

As a federal student loan borrower, you may qualify for general forbearance for Direct Loans, Federal Family Education Loans (FFEL), and Perkins Loans. Some of the qualifying reasons are:

- Financial hardship

- Medical expenses

- Change in employment (loss of job, working less) that causes economic hardship

Mandatory forbearance may be available for Direct Loans and FEEL program loans. You may be eligible for one of these reasons:

AmeriCorps: You serve in an AmeriCorps position for which you earned a national service award.

U.S. Department of Defense Student Loan Repayment Program: You qualify for partial repayment of your loans under this program.

Medical or dental internship or residency: You serve in one of these programs and meet specific requirements.

National Guard Duty: If a governor activates you, and you are not eligible for military deferment.

Student loan debt burden: For Direct Loans, FEEL program loans and Perkins Loans. In this case, the total amount you owe each month for all the federal student loans you received is 20% or more of your total monthly gross income, for up to three years.

Teacher loan forgiveness: For those who perform an eligible teaching service.

Coronavirus and Student Loan Forbearance

When the pandemic hit, it became harder for many students to repay their loans. As a result, the government initiated the Cares Act to provide some relief.

According to the Federal Student Aid, on Feb. 1. 2024, all federal student loan payments and collections were put on pause. And, the interest rate set at 0% due to the financial impact of COVID 19. President Biden signed an executive action on his first day in office to keep this relief going.

That said, if it’s possible for you to make payments, it could help you pay off your loan faster and lower the total cost of your loan over time.

What are the Differences between Federal Student Loan Forbearance vs Private Student Loan?

Both federal student loan forbearance and private student loan forbearance are short term ways to cope with lack of funds to repay a loan. You should contact either loan servicer right away if you are having trouble making payments so as not to default.

In the case of federal student loans, forbearance is usually granted for 12 months at a time and may be renewed for up to three years. The law mandates conditions and payment amounts for some types of these loans.

For example, due to COVID 19, the law set the interest rate at 0% as of 2021 and studentaid.gov updates the site as changes unfold. Unpaid interest is capitalized only on Direct Loans and Federal Family Education Loan FFEL Program loans, but never on Federal Perkins Loans.

Private lenders such as Sallie Mae may offer forbearance if you request it. The period may go to 12 months, but many lenders may not offer renewal. Each lender sets different conditions and amount for private student loans. Interest rates may vary too.

What are the Differences between Student Loan Deferment vs Forbearance?

Both deferment and forbearance allow you to temporarily postpone or reduce your federal student loan payments. You have to request both and wait for a yes or no from the lender.

The main difference is if you are in deferment, no interest will accrue to your loan balance. If you are in forbearance, interest does accrue on your loan balance.

Student loan deferment is a temporary postponement of payment on a loan that is allowed under certain conditions and during which interest does not tend to accrue on. The following student loans may qualify for deferment:

- Direct Subsidized Loans

- The subsidized portion of Direct Consolidation Loans

- Subsidized Federal Stafford Loans

- The subsidized portion of FFEL Consolidation Loans

- Federal Perkins Loans

All other federal student loans that are deferred will continue to accrue interest. You must still make payments until you receive a confirmation that your request is granted. Otherwise, you may risk delinquency (being late for even one day) and default (being late for 90 days or more).

According to the Federal Student Aid, being in default could affect your credit score as the loan servicer will report delinquency to 3 major national credit bureaus. Credit score matters if you ever need to finance a house, car, rent an apartment, etc.

How is this different from forbearance? A forbearance is a period during which your monthly loan payments are temporarily put on hold or reduced. Your lender may grant you one if you want to make payments but have a qualifying reason that explains you cannot afford to do so.

During forbearance, principal payments are postponed, but interest continues to accrue. Unpaid interest that accrues during the forbearance will be added to the principal balance (capitalized) of your loan(s), increasing the total amount you owe.

Different Types of Student Loan Deferment

How long are student loans deferred and getting deferment extension vs forbearance? Forbearance may last up to one year with the possibility to renew. Deferment periods vary and depending on the qualifying reason:

Cancer Treatment Deferment: You may be eligible during cancer treatment and for the 6 month period after it ends.

Economic Hardship Deferment: You may qualify for up to 3 years deferment if you receive a means tested benefit such as welfare. You may be eligible if you work full time but your earnings are below 150% of the poverty guideline for your family size and state. If you serve in the Peace Corps, this is another reason.

Graduate Fellowship Deferment: If you’re enrolled in an approved program that provides financial aid to graduate students.

In School Deferment: This deferment tends to be automatic. As a rule, to be eligible, you must be enrolled at least half time at an eligible college or career school. If you’re a graduate or professional student with a Direct PLUS Loan, you may qualify for an extra 6 months once you stop being enrolled at least half time.

Military Service and Post Active Duty Student Deferment: For this deferment, you must be on active duty military service tied to a war, military operation, or national emergency. If you’ve completed eligible active duty service and grace period you may also qualify.

Parent PLUS Borrower Deferment: This deferment is for the parent who received a Direct PLUS Loan to help pay for their child’s education. The student you took out the loan for must be enrolled at least half time at an eligible school.

Rehabilitation Training Deferment: For those enrolled in an eligible career, mental health alcohol or drug abuse rehab training program.

Unemployment Deferment: This deferment may be available for up to three years. It is for those who receive unemployment benefits and are seeking but unable to find full time work in their job search.

Private Student Loan Deferment vs Forbearance

It may be possible to defer your student loans or request a period of forbearance from a private lender. Each lender may set different terms and conditions but you typically have to request it and get their approval. Unlike federal loans, private ones are not included in the CARES Act.

Here’s an example with Sallie Mae student loans. If you request a deferment, Sallie Mae won’t ask you to make principal and interest payments while you’re in school or during your internship, clerkship, fellowship, or residency.

During deferment, your Sallie Mae loans return to the repayment option you chose when you took them out (i.e., interest, fixed, or deferred). That means if you were making either monthly interest only or fixed payments when you first took out your loan, you continue to make those throughout your deferment period.

That said, when you defer, interest grows while you’re in school, and increases your total loan cost. So, making any extra interest payments could lower this balance.

Is There a Difference between Student Loan Forgiveness vs Forbearance?

While loan forgiveness and forbearance help manage loans and payments, they are very different. Forbearance is short term only. Forgiveness, cancellation and discharge of your loans mean you no longer owe or have to repay part or all your loan.

There are various types of forgiveness, cancellation, and discharge available for the different kinds of federal student loans. If you are eligible, it may help your credit score and have a zero loan balance. Compared to forbearance where you still owe and risk being in default.

Different Types of Student Loan Forgiveness

PSLF is for eligible full time employees of U.S. federal, state, local, or tribal governments or nonprofits. There’s a specific form to fill out in order to request and potentially receive, forgiveness.

It forgives the outstanding balance on Direct Loans. You must make 120 qualifying monthly payments under a qualifying repayment plan. You also must work full time for a qualifying employer.

Teacher Loan Forgiveness: This type of federal student loan forgiveness awards up to $17,500 in forgiveness. It may be available for Direct Loans and FEEL Program loans. You may be eligible if you teach full time for 5 consecutive academic years. This work must be in a low income elementary, secondary or educational service agency.

Closed School Discharge: If the school you attend closes while you’re enrolled or soon after you withdraw, you may be eligible for discharge of your federal student loan. Eligible are Direct Loans, FEEL loans and Perkins Loans.

Federal Perkins Loan Cancellation and Discharge: The basis for this kind of cancellation is eligible employment or volunteer service and the length you were in the position. Teachers, nurses, military personnel and other professionals from federally approved jobs that may qualify.

Total and Permanent Disability Discharge: This option may be available for holders of Direct Loans, FEEL Program loans, and Perkins Loans. You may qualify if your disability is total and permanent. In addition, you may be eligible for a discharge on TEACH Grants.

Discharge Due to Death: Federal student loans are discharged upon death. Whether of the student on whose behalf a PLUS loan was taken out. Or, of the borrower. It may be available for Direct Loans, FEEL Program loans, and Perkins Loans.

Bankruptcy: It is rare, but you may be able to have your federal student loan discharged after you declare bankruptcy. This is not automatic and may be available for Direct Loans, FEEL Program loans, and Perkins Loans.

Borrower Defense to Repayment: You may be eligible for discharge of federal Direct Loans for this reason if you took out loans to attend a school (let’s say the school was a scam). And the school did or failed to do something related to your loan or the education you took out the loan to pay for.

False Certification Discharge: This is for those whose school falsely certified your eligibility to receive a loan. Direct Loans and FEEL loans to be exact.

Unpaid Refund Discharge: For Direct Loans and FEEL loans only. In this case you withdrew from school and the school didn’t make a required return of loan funds to the loan servicer. If you do qualify it is likely for the portion of your federal student loan(s) that the school failed to return.

Alternate Student Loan Repayment Options

Before you consider forbearance, there are alternative ways to repay federal and private student loans. You should assess each option to see which one you qualify for and is in your personal best interest.

Refinancing

If you have private student loans and qualify for a better interest rate, you might consider refinancing. Lower interest rates means you pay less each month. That said, not all lenders offer this option.

Consolidation

If you have a few student loans, you may be able to combine them into one loan with a fixed interest rate based on the average of the interest rates on the loans being consolidated. For example, a Direct Consolidation Loan allows you to blend multiple federal education loans into one loan at no cost to you.

Income Driven Repayment Plans

IDRs aim to make your student loan debt easier to manage by lowering the amount you pay each month. These plans base your monthly student loan payments on your income and family size.

The federal government offers 4 plans but private loans don’t qualify for any of them.

- Revised Pay As You Earn Repayment Plan (REPAYE Plan): Generally 10% of your discretionary income.

- Pay As You Earn Repayment Plan (PAYE Plan): Generally 10% of your discretionary income. But never more than the 10 year Standard Repayment Plan amount

- Income Based Repayment Plan (IBR Plan): If you are a new borrower on or after July 1, 2014, the terms are the same as the PAYE Plan. But if you are not a new borrower on or after July 1, 2014, it tends to be 15% of your discretionary income and never more than the 10 year Standard Repayment Plan amount.

- Income Contingent Repayment Plan (ICR Plan): Whichever is less than 20% of your discretionary income. Or, what you would pay on a repayment plan with a fixed payment over a span of 12 years, adjusted to your income.

What Option is a Good Choice to Help Pay off Student Loans?

There are a few tactics that may help pay off a student loan and hopefully avoid either forbearance or deferment.

- Try to make extra payments when possible

- Set up automatic payments so you don’t forget

- Pay off capitalized interest because it brings your balance up

- Use any gift money to repay your student loan

If you did all these things and find yourself unsure, you should first contact your loan lender. The lender could inform you which option you qualify for and how to request it plus other next steps.

Remember that both forbearance and deferment allow you to reduce or postpone payments in the short term only. While forgiveness is ideal (who doesn’t want the magic wand that takes debt away?) you may not qualify at all.

Forbearance on federal student loans now has favorable terms with the 0% interest which means your total amount owed won’t go up. There’s also no impact on your credit score. Before you choose this route, compare with an IDR. These plans tend to be more long term.

On the other hand, if you qualify for a deferment, interest grows and adds up which may make it that much harder to repay. This could set you up for delinquency and default which is not ideal and affects your credit score. Still have questions? Check out our section on student loans.